Questions and Answers: Tackling non-performing loans to enable banks to support EU households and businesses

What are non-performing loans (NPLs) and how do they affect the economy and the lives of people?

Non-performing loans (NPLs) are bank loans that are:

- subject to late repayment (i.e. 90 days past due); or,

- unlikely to be repaid by the borrower, if, for example, the borrower faces financial difficulties.

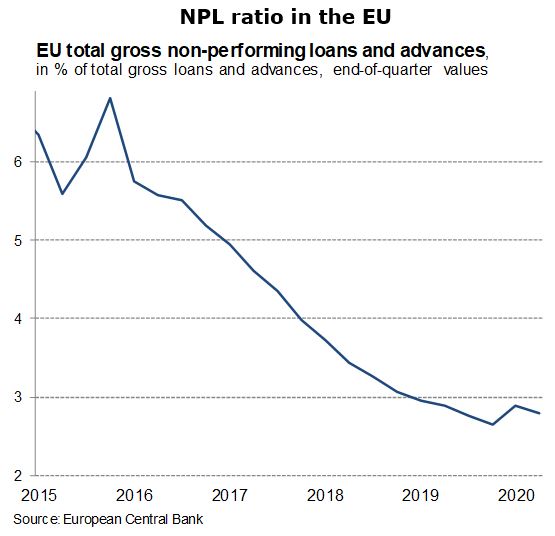

The 2008 financial crisis, and the subsequent recession, made it very difficult for many Europeans to pay back their mortgages or loans. As a result, this led to a build-up on NPLs in banks. This was particularly acute in some EU Member States. While at the end of 2016, NPLs represented only 5.1% of the EU's total amount of bank loans, this ratio varied from 1% to 46% among Member States.

This build-up of NPLs slowed down bank lending, economic growth and threatened financial stability.

What do the latest available figures on NPLs show?

Thanks to decisive action and comprehensive measures taken at national and EU level, such as the Action Plan to Tackle Non-Performing Loans in Europe (July 2017), and on the back of more favourable economic conditions, the level of NPLs (along with other risks) in the banking sector in Europe has come down substantially in recent years. We are clearly not in the same situation as we were during the previous financial crisis.

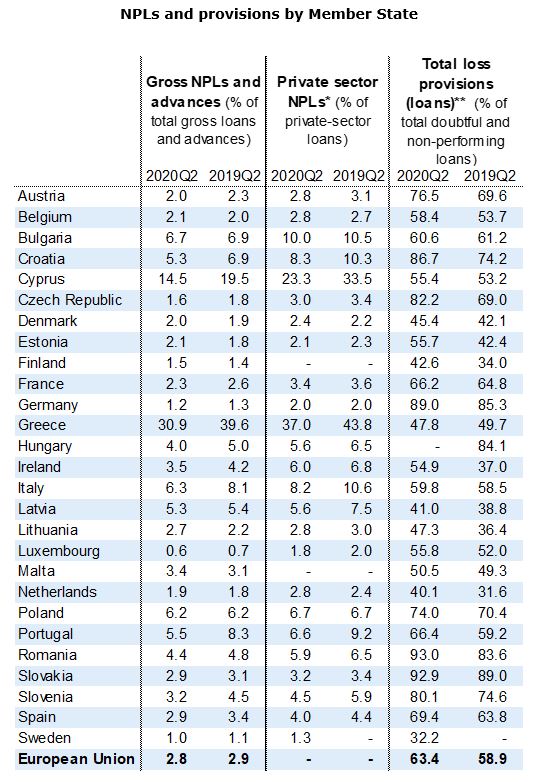

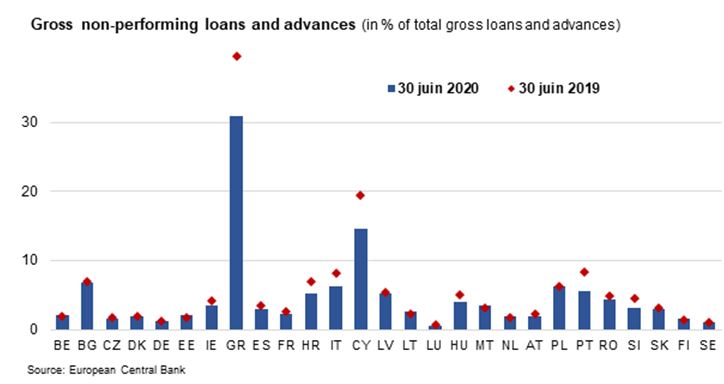

However, NPL levels and ratios (i.e. NPLs in relation to total loans) continue to vary greatly across Member States and banks. High NPL ratios remain a significant challenge in some banks and weigh considerably on their performance. Therefore, decreasing the number of NPLs has remained one of the EU's key priorities in order to reduce risk further in the EU's banking sector.

Before the coronavirus outbreak, the level of NPLs had reduced substantially across the EU. In Q4 2019, the NPL ratio reached a low point, after a continuous downward trend since 2016, amounting to 2.6%.

How is coronavirus affecting the build-up of NPLs?

The latest figures for the first half of 2020 revealed a halt in the downward trend in NPLs driven mainly by reduced NPL sales and banks' restructuring activities, as well as new defaults. As a result, the NPL ratio, covering all EU banks, has unfortunately started to rise again. At the end of Q2 2020, the NPL ratio for all EU banks was 2.8% (+0.2 p.p. compared to Q4 in 2019).

Due to the coronavirus pandemic, households and businesses in the EU, in particular small and medium-sized enterprises (SMEs), have encountered financial problems. In practice, this means that they experience, or are likely to experience, difficulties in the repayment of their loans. Depending on how the crisis evolves, the number of NPLs might be on the rise in the coming months. This may prevent banks from continuing to lend to households and businesses, which in in turn would lead to a delay in the EU's economic recovery, creating a tangible and lasting effect on the real economy.

What is the state-of-play of the ECOFIN 2017 Action Plan?

In response to the increase of NPLs in the aftermath of the 2007-2008 financial crisis, the ECOFIN Council adopted an Action Plan to tackle NPLs in Europe in July 2017.[1]

Following this, the Commission announced in October 2017 a comprehensive package of measures to reduce the level of NPLs in the EU in a Communication on Completing the Banking Union.

The package, presented by the Commission in March 2018, set out a comprehensive approach with a mix of complementary measures:

- a proposal for a Regulation introducing the statutory prudential backstop ensuring sufficient loss coverage by banks for NPLs (adopted in April 2019);

- a proposal for a Directive on credit servicers, credit purchasers and the recovery of collateral, which aimed at fostering the development of secondary markets for NPLs and improving the enforcement of loans secured by collateral. This is currently under discussion in the European Parliament;

- a technical blueprint for how to set up a national asset management company (AMC).

The Council has agreed upon a mandate for negotiations with the European Parliament on the Directive on Credit Servicers and Credit Purchasers since March 2019 and for the Directive on the accelerated extrajudicial collateral enforcement mechanism since November 2019. These texts are currently being discussed in the European Parliament. Once the European Parliament formalises its position, inter-institutional negotiations could start. Deliberations in the European Parliament on both aspects should be taken up as a priority. This is of paramount importance if the EU is to successfully tackle NPLs across Europe, especially given the expected impact of the coronavirus pandemic.

What has the Commission done so far this year to tackle NPLs, given the coronavirus crisis and what will it do going forward?

The Commission has taken, or proposed, actions to tackle the current crisis by providing greater flexibility in the requirements applicable to Member States, banks and corporates. For NPLs, this includes:

- The Banking Package presented in April 2020 provides substantial short-term support by introducing flexibility in certain EU rules, such as:

- The rules on how banks assess the risk that a borrower will not repay a loan in a sudden economic crisis, such as the fallout caused by the coronavirus pandemic, and the effect this has on the amount of provisions the bank needs to make for any possible losses;

- The prudential rules on the classification of non-performing loans where relief measures such as moratoria or public guarantee schemes have been provided;

- The accounting treatment of delays in the repayment of loans (the Interpretative Communication included in the Banking Package clarifies the impact of relief measures, such as moratoria on the accounting treatment of loans).

- The Capital Markets Recovery Package, which aimed to encourage greater investments in the economy, allow for the rapid re-capitalisation of companies and increase banks' capacity to finance the recovery, notably by removing regulatory obstacles to the securitisation of NPLs.

The Commission also facilitated the agreement of a list of ‘best practices' between the financial sector, and consumer and business organisations, to help further mitigate the impact of the coronavirus pandemic. It sets out concretely how different financial market participants can support citizens and businesses throughout the crisis.

Following up on this agreement, the Commission intends to organise a new roundtable meeting to take stock of relief measures offered during the first wave of the pandemic in Member States, as well as to discuss to what extent the best practices were applied on the ground, and whether they proved useful in helping consumers and businesses make use of national relief measures.

What is the Commission proposing today and why?

By providing liquidity to households and businesses in difficulties, banks and other credit institutions play an important role in mitigating the impact of an economic crisis. At the current juncture, EU regulators and policy makers need to make sure that banks are able to sustain the flow of credit to businesses and households, as the pandemic is mostly hitting firms in sectors that are otherwise generally viable, and that will likely rebound once the pandemic subsides.

Today's Communication aims to ensure that the necessary tools are in place to deal with a possible increase in coronavirus-related NPLs. By doing so, the economic recovery can be supported to the benefit of households and business across the European Union.

Drawing lessons from the last economic crisis, the Commission is proposing a complementary component to the initial 2017 Council Action Plan in order to address coronavirus-related NPLs as early as possible and to prevent a renewed build-up of NPLs on banks' balance sheets. The Communication includes the following key measures:

- Strengthening the development of secondary markets for NPLs while ensuring a high degree of debtor protection across the Single Market. In order to improve the functioning of secondary markets, better quality and comparability of NPL data across the EU is required, through data standardisation. Furthermore, in order to consolidate data infrastructure, the creation of a data hub at European level dealing with post-trade information would deliver additional market transparency, which is the key to rendering markets more efficient. The Commission would also aim at developing guidance for sellers of NPLs, including recommendations on what entails a ‘best execution' sales process, while ensuring further strengthened protection for debtors. The Commission would also aim to address remaining regulatory impediments to NPL sales by banks.

- Supporting Member States in the set-up of national AMCs – if they wish to do so – and exploring the merits of establishing a network of national AMCs at EU level. This would build on the existing Blueprint guidance for establishing national AMCs. AMCs can be very effective in freeing banks from the burden of high NPLs, as examples after the financial crisis have shown. In addition, enabling a cross-border network of national AMCs at EU level could amplify the collective effectiveness of national AMCs across the EU. It could facilitate their cooperation and create valuable synergies. National AMCs could exchange best practice experience, enforce data and transparency standards and, where necessary, coordinate creditor actions;

- Converging insolvency frameworks across the EU, either through a legislative or a non-legislative proposal. This would also improve the efficiency of these proceedings within the Single Market.

- Outlining the precautionary tools provided by the EU bank crisis management and State aid frameworks, in the context of the coronavirus crisis, as set out in the March 2020 Communication on the Temporary Framework for State aid measures to support the economy.

How will you ensure consumer protection?

In July 2020, the Commission welcomed the ‘best practices' agreed by the financial sector, and consumer and business organisations, that outlined concretely how different market participants can support citizens and businesses throughout the crisis[2]. The Commission will continue to maintain a fair, robust and consistently enforced consumer protection regime.

Today's Communication strives to achieve an important balance between enabling banks to recover the value of loans they provided, while protecting European citizens and business from reckless credit enforcement in the context of a sharp economic recession.

The Communication complies with existing legal standards, especially those related to borrower and data protection:

- The development of secondary markets and the enhancement of the functioning of the insolvency and debt recovery frameworks ensure the preservation of rights and obligations of debtors.

- The improvement of market transparency and access to information of NPL markets will respect all relevant data protection rules regarding debtors.

- Finally, the support provided to the economy will benefit households and businesses hit by coronavirus.

As outlined in the proposed Directive on Credit Servicers, Credit Purchasers and the Recovery of Collateral, credit servicers need to demonstrate an organisational structure that allows them to comply with borrower rights and data protection. They are also required to set up procedures to deal with vulnerable groups and borrower complaints and they need to inform borrowers about the supervisors that follow up on borrowers' complaints. Credit servicers are not allowed to request fees to deal with complaints. Supervisors are empowered to review this, to follow up on borrower complaints and to apply sanctions if necessary.

Furthermore, credit purchasers need to respect consumer rights as provided for by the Mortgage Credit Directive and the Consumer Credit Directive and have the obligation to inform supervisors whether they enforce the debt directly or delegate this to a dedicated credit servicer. If the loan purchaser is from a third country, it is obliged to use an EU-supervised loan servicer.

What are templates and why do you want to make them mandatory?

Data templates provided by the European Banking Authority (EBA) are an essential basis for developing a common data standard at European level for NPL transactions on secondary markets. In short, these templates improve data comparability and quality. The EBA's templates have not yet been widely used by market participants, due to their voluntary nature and rather complex structure.

The Commission is considering making EBA templates mandatory, although a gradual approach would seem appropriate. Some flexibility should also be granted: banks should not be penalised if they do not have non-essential data.

Furthermore, in order to improve the benefits of these templates, the Commission would mandate the EBA to review the templates based on thorough consultation with relevant market participants and regulators in order to distinguish critical and non-critical parts of the templates.

Are you proposing the creation of a central data hub? What would be its purpose?

In order to enhance market transparency at a granular level, the Commission considers that there would be merit in establishing a central data hub at EU level.

A central data hub could act as a data repository underpinning the NPL market. Such specialised repository infrastructures have been established in Europe in order to address financial stability issues, for instance to deal with the lack of transparency on derivatives transactions.

The hub would operate a regularly updated comprehensive electronic database, assess the information and provide access to market participants, notably credit sellers, credit purchasers, credit servicers, NPL sellers and private NPL platforms. It would collect and store anonymised data on NPL transactions that have taken place and provide such post-trade transaction details and sale prices to market participants.

The hub would therefore be a driver for enhancing market efficiency. It could help develop further data standardisation. It would allow market participants to compare transactions and gain insights into the actual pricing of assets and market liquidity on a systematic basis, thereby supporting price discovery on secondary markets.

Will there be a European bad bank?

Several factors would make it difficult to set up a single, European AMC. These include the diversity of NPL portfolios across Member States, and different national rules on restructuring, insolvency and collateral enforcement. The costs of setting up a European AMC could also be very high.

Nevertheless, AMCs could play an important role in the overall strategy to tackle the anticipated rise in NPLs caused by the coronavirus crisis. When properly designed and managed and accompanied by supporting policy measures, national AMCs can significantly contribute to Member States' efforts to tackle the NPL challenge. An AMC at Member State level brings a number of benefits to the national financial system.

Furthermore, important synergies could materialise if a large number of Member States established an AMC within their jurisdiction. In such circumstances, there would be a possibility to create a well-connected network of AMCs across the EU, which could facilitate substantial synergies and network externalities. When steered appropriately, this network would amplify the collective effectiveness of the national AMCs across the EU. It would bring about economies of scale and scope. However, the establishment of a national AMC remains voluntary. Member States are free to decide whether they would want to go down this path.

For More Information

Proposal for a Directive on credit servicers, credit purchasers and for the recovery of collateral

Commission STAFF WORKING DOCUMENT on AMC Blueprint Accompanying the document Communication from the Commission –

Second Progress Report on the Reduction of Non-Performing Loans in Europe

[1] See https://www.consilium.europa.eu/en/press/press-releases/2017/07/11/conclusions-non-performing-loans/.

[2] ‘Best practices in relation to relief measures offered to consumers and businesses in the context of the CORONAVIRUS crisis', 14 July 2020.

See: https://ec.europa.eu/info/sites/info/files/business_economy_euro/banking_and_finance/documents/200714-best-practices-mitigate-impact-pandemic_en.pdf.